The Rise of Banking-as-a-Service (BaaS): A New Layer of the Financial Stack

Learn how Banking-as-a-Service (BaaS) is transforming financial infrastructure, enabling embedded finance, and creating new business models.

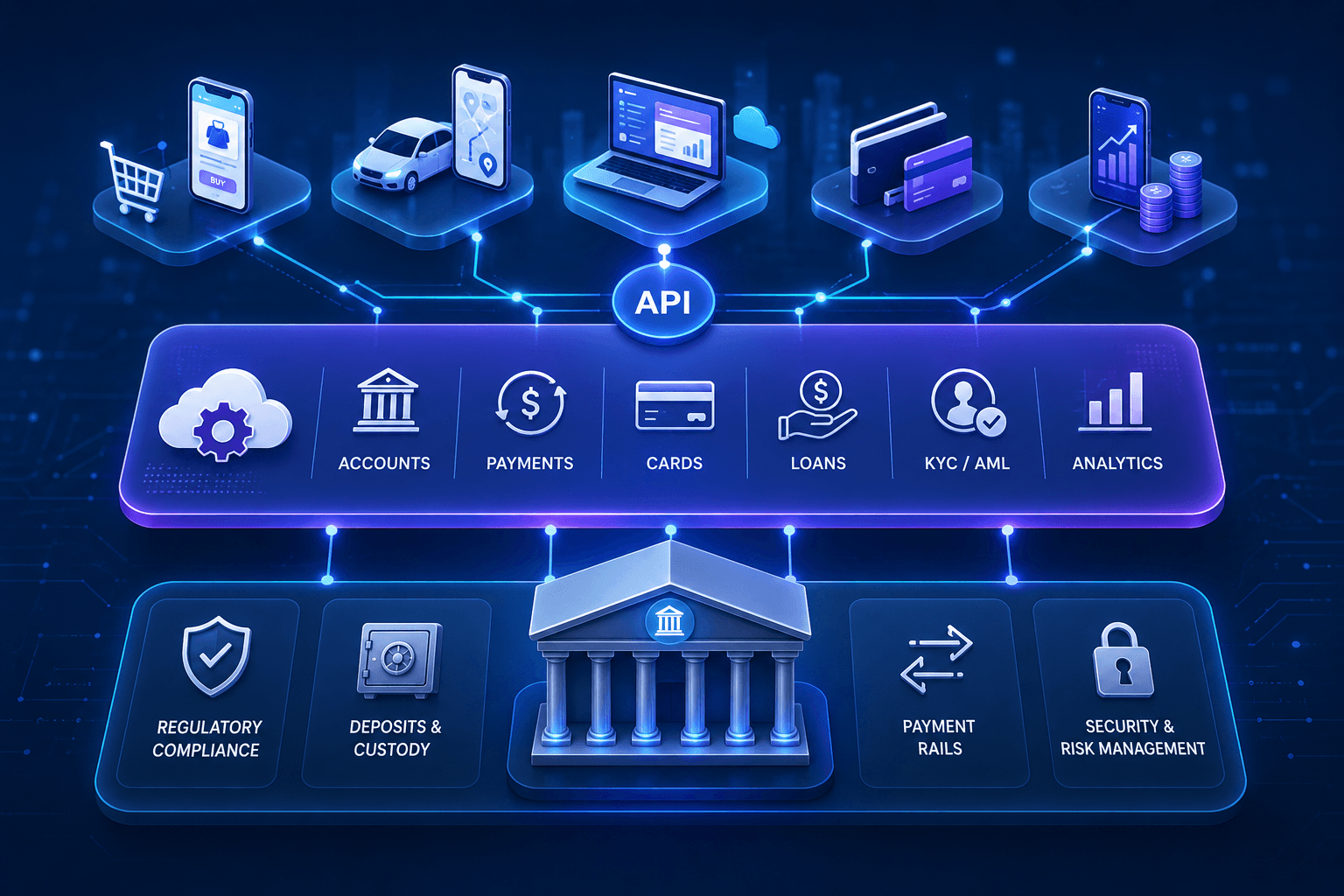

Banking-as-a-Service (BaaS) lets companies offer banking products without becoming banks themselves. Industry players and technology service providers define BaaS as an approach that enables non-banking enterprises to provide banking functionalities using financial institutions’ licensed facilities and application program interfaces (APIs).

BaaS providers have become an essential aspect of fintech. The BaaS model provides enterprises with an opportunity to incorporate services such as payment solutions, accounts, credit services, and card issuance without a need for banking licenses. Traditional banking institutions still handle regulatory issues and access to the payment rails while technology companies use APIs to develop customer-centric financial products.

How Banking-as-a-Service Operates Within Modern Finance

Banking-as-a-Service refers to how licensed banks work with technology partners by using the available digital infrastructure. Rather than developing new banking systems from scratch, firms can use bank functionality via BaaS API integrations.

Banking-as-a-Service works much like cloud computing. Just as companies rent computing infrastructure from cloud providers instead of building data centers, businesses can access banking infrastructure through BaaS providers instead of becoming banks. This allows organizations to launch financial products faster while avoiding the cost and complexity of building banking systems from the ground up.

It usually involves three primary entities. The banks take care of compliance and custody of customer money. Connectivity and access to banking features are provided by BaaS platforms. The business, in turn, uses the services for creating its own financial products. This model helps keep the product team away from regulatory processes and banking technologies.

Compared to conventional banking, it represents a completely different approach because, in the past, financial institutions owned not only the infrastructure but also handled customers directly. BaaS divides these tasks among different providers and enables companies to concentrate on their core competence.

Developments in cloud technology infrastructure have led to the emergence of BaaS. Advanced API technologies allow for real-time transactions, authentication, and payment processing through various platforms.

Embedded Finance Drives Demand for BaaS Platforms

The growth of embedded finance has created a demand for banking-as-a-service (BaaS). Customers now access financial products via shopping platforms, mobility applications, software products, and e-marketplaces besides using banking channels.

Banking-as-a-Service allows businesses to create financial products without setting up a banking institution. For example, a marketplace will provide bank accounts to sellers, a ride-hailing company will offer prepaid credit cards, and a software product provider will embed financial instruments for businesses in its platform.

This is an alternative solution that speeds up development because businesses do not have to design the entire bank infrastructure on their own. For founders, this means launching financial products in months instead of spending years building banking infrastructure.

Market participants emphasize that there are new demands from customers regarding financial services. People are now seeking financial solutions that are embedded in popular apps that they use in their daily lives.

Technical Infrastructure Behind Banking-as-a-Service

Behind each BaaS offering is a set of APIs, cloud-based technology, and compliance solutions that permit the delivery of financial services within applications which are not necessarily banks.

In BaaS system, API gateways handle requests from various parties for transactions and data exchange purposes. Identification systems help to address KYC requirements. Anti-money laundering systems help track transactions.

Real-time payment systems also play a vital role in the operation of BaaS models by facilitating real-time movement of funds. Many of the BaaS vendors use the microservices approach, in which the bank-related services are separated into distinct microservices. This enables the vendor to change or scale any particular service without impacting the whole solution.

The advantage of adopting this approach is that individual banking functions work independently and at the same time in coordination with other services. Information security is one of the key elements of BaaS. In addition to regulatory compliance, encryption and authentication measures are used.

Banks and Technology Firms Expand Financial Partnerships

Banking-as-a-Service is the result of greater cooperation between banks and technology providers. In such an approach, banks have access to new distribution channels, whereas companies have the opportunity to offer banking products without undergoing all the bureaucracy required of becoming a financial institution.

Businesses that adopt BaaS also depend on banking partners and infrastructure providers. Changes in regulation or service availability can affect product operations. As a result, companies often evaluate provider reliability, compliance capabilities, and long-term partnership strategies before launching financial products.

As innovations in digital financial services progress, it can be assumed that BaaS solutions will still be included in the FinTech ecosystem. The ability of BaaS to link banking infrastructure and digital financial products makes it a valuable element of the contemporary delivery of financial services.

As more companies look to add financial services without becoming financial institutions, BaaS is becoming a practical way to launch new products, generate revenue, and reduce development timelines.